The Pipeline That Looked Like a Market Problem And Wasn't

A real example of how a structural diagnosis identified the specific breakdowns causing inconsistent deal flow and what a working system looks like once they are corrected.

4 min read

THE SITUATION

The investor had been active for several years. He was not a beginner. He had closed deals, built relationships with brokers and wholesalers, and understood his target market. By most measures, he was an experienced operator.

But his pipeline was inconsistent in a way he could not explain.

Some months he was reviewing four or five opportunities. Other months his inbox was empty. When deals did come in, a significant portion of his time went to evaluating opportunities that were not aligned with his criteria, deals he knew within minutes were not fits, but that he reviewed anyway because they were what was available.

When a strong deal came in, he was sometimes not positioned to act quickly. The evaluation process took longer than it should. By the time he was ready to move, the window had closed.

He had attributed this to the market. The market was tighter than it had been. Competition was higher. Good deals were harder to find. The market was part of the story. It was not the whole story.

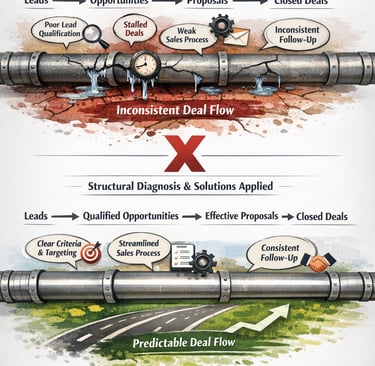

WHAT THE DIAGNOSIS FOUND

The review of his deal flow identified four specific structural breakdowns, none of which were caused by the market.

1. His deal sources were not producing consistently because they were not being maintained consistently He had relationships with six wholesalers and three brokers. In practice, three of those relationships were active and three were dormant. The dormant ones had been built during periods of high activity and had atrophied during slower periods. He was not managing his source relationships as a system, he was reacting to whoever reached out.

The result was that his pipeline was only as active as his most active sources, and those sources had no reason to prioritize him over buyers who communicated more consistently.

2. He had no filtering mechanism When a deal came in, it entered a mental evaluation process that had no defined criteria and no defined sequence. Every deal got roughly the same amount of initial attention regardless of how well it aligned with his investment criteria. This meant that a deal that was immediately not a fit consumed the same mental bandwidth as a deal that was genuinely worth evaluating.

Over time, this created fatigue. He was spending real time and attention on deals that he knew were not fits, not because he lacked judgment, but because he had no system that allowed him to quickly separate them.

3. His decision process had no documented sequence When a deal that was a potential fit arrived, the evaluation process began from scratch each time. There was no defined sequence of questions, no consistent order of analysis, and no clear threshold at which a deal moved from initial review to serious consideration. This made every evaluation longer than it needed to be and introduced inconsistency in which factors received attention first.

4. His pipeline reset after every close Each time he closed a deal, his attention shifted entirely to that deal's execution. The sourcing and evaluation activity stopped. By the time the deal was stabilized and his attention was available again, his source relationships had cooled and his pipeline was empty.

This was the most consequential structural problem. It meant that every deal cycle started from zero.

WHAT CHANGED

Four specific structural corrections were made.

A source maintenance schedule was established, not a heavy process, a minimal one. Each active source received a brief touchpoint on a defined cadence. Dormant sources were reactivated with a specific outreach. The standard for what constituted an active relationship was defined clearly.

A deal filter was built. A one-page set of criteria, asset type, geography, price range, minimum condition requirements, minimum return threshold, was documented and used as the first pass on every incoming deal. Deals that did not meet the filter were declined immediately. This took the average initial evaluation from fifteen minutes to under two.

A decision sequence was documented. The order of analysis was fixed: filter first, then financial model, then structure review, then decision. This eliminated the variability in the evaluation process and reduced the time from first look to decision by roughly half.

A pipeline maintenance protocol was added to every deal's execution checklist. While a deal was in progress, source maintenance activity continued on a reduced schedule. The pipeline did not stop while execution was happening. It ran at a lower intensity.

WHAT HAPPENED

Within six weeks, deal flow became measurably more consistent. Not because more deals existed in the market, the market had not changed. But because the system was now producing a consistent stream of filtered, relevant opportunities from maintained relationships, evaluated through a defined process.

The investor was spending less time reviewing deals that were not fits. The deals that were fits were reaching a decision faster. And when a deal closed, his pipeline did not reset to zero.

The market affects volume. It does not explain why some investors maintain consistent flow while others stall. The difference is almost always structural.

WHAT THIS ILLUSTRATES

Deal flow problems feel like sourcing problems. They are almost never sourcing problems. They are system problems, specifically, the absence of a structure that controls how deals enter the pipeline, how they are filtered, and how the pipeline is maintained through the natural cycles of execution and recovery.

An investor who solves the sourcing problem by finding more sources is adding volume to a broken system. More deals flowing into an unstructured pipeline creates more noise, not more results.

Structure is what turns access into consistent opportunity.

If your pipeline is inconsistent and you want to understand exactly where the structure is breaking down, this is where that diagnosis starts.

© 2027. All rights reserved. Netrix Enterprise LLC 3343 Peachtree Rd Atlanta GA 30326 - Privacy Policy - Terms And Conditions - Referral and Compensation Earnings and Results Disclaimer